The Premium

For the first time since 1996, the world's central banks hold more gold than American debt. The number is a footnote. The motive is the hinge.

by Lawrence Winnerman

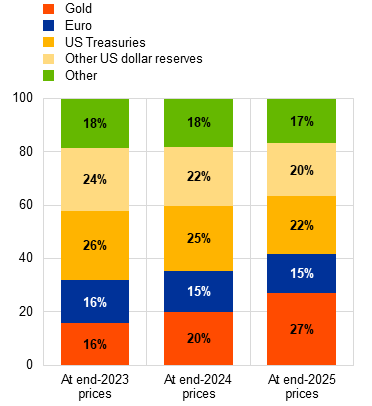

On Tuesday, June 2, the European Central Bank published its annual report on the international role of the euro. There was no press conference worth the name. No emergency session, no market halt, no cable-news chyron. The news was a chart: at the end of 2025, gold made up 27 percent of the world’s official reserve holdings, and United States Treasury securities made up 22.

The Thirty-Year Round Trip

The last time the world’s central banks held more gold than American government debt was 1996.

I’m old enough to remember thirty years ago. Bill Clinton was campaigning on a bridge to the twenty-first century. The Motorola StarTAC was the future of telephones. The World Wide Web had roughly forty million users, most of whom were listening to it dial. And the global financial system was completing a long migration into a single, settled consensus: the safest place on earth to store national wealth was a loan to the United States of America.

That consensus was so total that within three years, the United Kingdom began selling off its gold—roughly 395 tons of it, auctioned between 1999 and 2002 at an average price near $275 an ounce, a bottom so perfectly timed that traders still call it Brown’s Bottom, after the chancellor who ordered the sale. The logic was impeccable: gold paid no interest; gold was a relic.

Treasuries were liquid, dollar-denominated, and backed by the most credible institutional machinery in human history. Why hold a metal when you could hold a promise?

Gold finished 2025 at $4,322 an ounce.

This essay is about what happened to the promise.

Let me deflate my own balloon before someone does it for me, because the doom-flavored version of this story is wrong, and the wrongness matters.

Gold did not overtake Treasuries because central banks dumped American debt in a panic. Most of the inversion is arithmetic: gold’s price rose 65 percent last year, so its share of reserve portfolios ballooned even where nobody bought a single additional bar. The physical buying actually slowed—850 tons in 2025, down from more than 1,000 tons in each of the three years prior. And dollar-denominated assets, taken together, still make up 42 percent of global reserves, the largest share of anything.

The dollar is not collapsing. Anyone who tells you it is collapsing is selling you a newsletter or a bunker.

If that were the whole story, this would be a footnote.

It is not the whole story.

The story is in the surveys, where central bankers say quietly what they would never say at a podium.

In 2023, UBS asked the world’s reserve managers whether they worried that their US assets could be frozen—seized, in effect, by the country that issued them. Fourteen percent said yes. Last year, 49 percent said yes.

Let’s stop here for a minute. These are not crypto evangelists or gold-bug pamphleteers. Reserve managers are the designated worriers of the world economy—careful, gray, institutionally conservative people whose entire professional function is to make sure the national savings still exist next quarter.

In two years, the share of them who believe the United States might confiscate their holdings went from one in seven to one in two.

They learned this fear honestly.

In February 2022, after the invasion of Ukraine, the United States and its allies froze roughly $300 billion of the Russian central bank’s reserves. And here is where the easy version of this essay—the one with a single villain in it—falls apart, because that decision was made by a Democratic administration, with broad allied support, in response to a genuine atrocity. It was arguably the right call. It was certainly an effective one.

But sanctions of that kind work exactly once, and the price of using the weapon is that everyone watching learns the weapon exists. Every finance ministry from Beijing to Brasília absorbed the same lesson on the same afternoon: a Treasury bond is a promise, and promises have conditions.

None of this requires villainy. It requires only momentum. Each administration found the dollar too useful a lever not to pull—sanctions here, tariffs there, a freeze when the cause was just. Each pull was rational in isolation. The cumulative effect was to teach the world that the risk-free asset carries a risk after all, and the risk is us—the irrational, 800-pound gorilla that is the United States of America.

You might not be able to trust us with the Bomb, and you probably can’t trust us with the entire basis of your national economy either.

Then came the acceleration. In April of this year, one month after American and Israeli strikes on Iran, the surveyors went back to the reserve managers. Seventy percent now named geopolitics as the single most significant risk they face—ahead of inflation, ahead of cyberattack, ahead of everything.

A third said it would be the dominant factor guiding their reserves for the next five years. In March alone, the value of Treasuries held in custody for foreign officials at the New York Fed fell by $82 billion, to its lowest level since 2012.

Here is the sentence the chart in the ECB report is actually saying: the most conservative institutions on earth have begun buying insurance against the United States.

Nobody buys insurance against a counterparty they trust.